Dienstag, 30. Dezember 2008

The US housing bubble in historical perspective

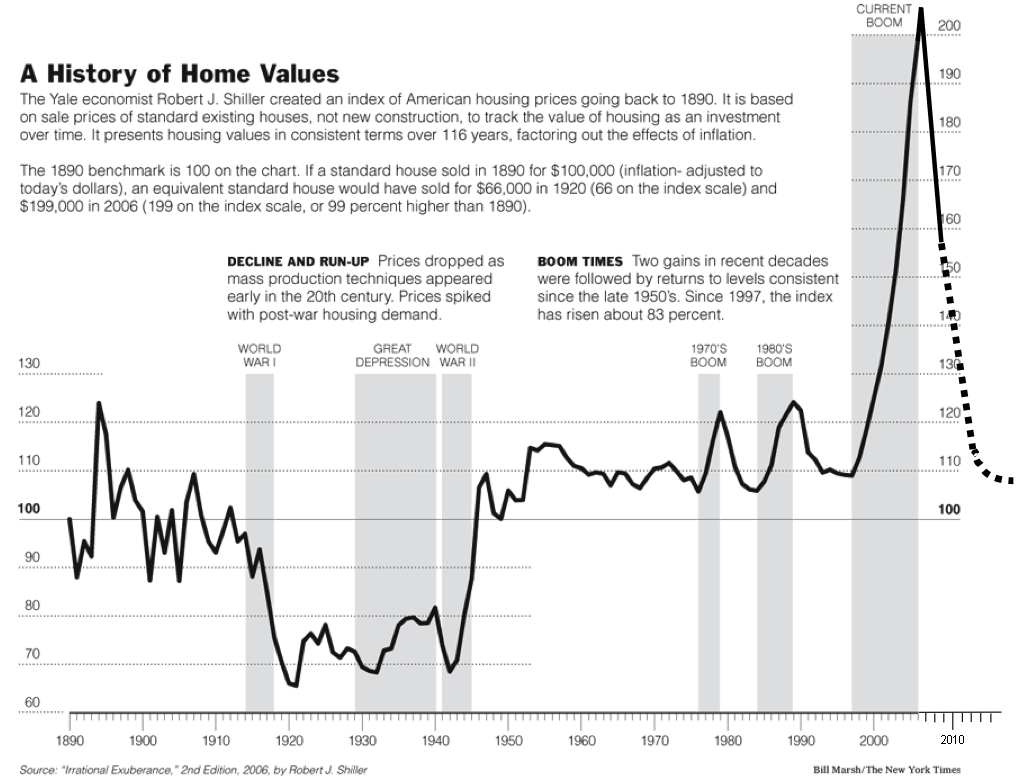

Blogger Barry Ritzholtz at The Big Picture presents a diagram with the long-term evolution of US housing prices according to the Case-Shiller index. The diagram shows the extreme overvaluation during the housing bubble that began in the late 90s and burst in 2007. The diagram also suggests that a further massive downward correction is unavoidable during the coming years.

Samstag, 27. Dezember 2008

Summers: A Stimulus Must Aim for Long-Term Results

Larry Summers, designated director of Barack Obama's National Economic Council, has published the first inside statement on Obama's fiscal stimulus package. The focus will be on investment:

Investments in an array of areas -- including energy, education, infrastructure and health care -- offer the potential of extraordinarily high social returns while allowing our country to address some long-standing national challenges and put our economy on a solid footing for years to come. more...

The stimulus package is supposed to create 3 million new jobs:

... more than 80 percent of these 3 million jobs will be in the private sector, including emerging sectors such as environmental technology. This is a bold goal. But economists across the political spectrum recognize that it is far less risky to stand firmly against the forces propelling our economy downward than to be timid in the face of a mounting crisis. more...For a skeptical view of the proposed stimulus package, see this entry in Greg Mankiw's blog with further links.

Mittwoch, 24. Dezember 2008

Schuldenverbot im Grundgesetz?

Hans-Jürgen Papier, Präsident des Bundesverfassungsgerichts, warnt in seinem heutigen Interview mit dem Hamburger Abendblatt vor einer fortwährenden Expansion der staatlichen Aufgaben und Ausgaben. "Wenn die Schuldenlast immer größer wird, geht insbesondere in Krisenzeiten die Lenkungs- und Gestaltungsfähigkeit des Staates verloren." Im Hinblick auf die aktuelle Finanz- und Wirtschaftskrise und das geplante schuldenfinanzierte Konjunkturpaket sagt er: "Die Begrenzung der Staatsverschuldung ist vom Bundesverfassungsgericht als ganz zentrale Aufgabenstellung bewertet worden. ... Das Ziel der Haushaltskonsolidierung sollte nicht aus den Augen verloren werden." Auf die Frage, welche Schuldenbremse er sich vorstellen könnte, antwortet er: "... etwa die Verankerung eines absoluten Schuldenverbots im Grundgesetz, das nur in wirklichen Notzeiten durchbrochen werden darf, gegebenenfalls mit qualifizierter Parlamentsmehrheit."

Dazu zwei Einwürfe (von ökonomischer Seite) zur Anregung einer Diskussion:

Dazu zwei Einwürfe (von ökonomischer Seite) zur Anregung einer Diskussion:

- Die herrschende Meinung unter Ökonomen (= Mainstream-Ökonomie) sieht das anders; sie befürwortet, dass der Staat in der Krise genau nicht auf Haushaltskonsolidierung setzt, sondern sich antizyklisch verhält.

- Auch die geltenden Regeln der EU (Stabilitäts- und Wachstumspakt) sehen vor, dass ein Staat im Falle einer schweren Rezession - die ja nach der gegenwärtigen prognostischen Gemengelage tatsächlich droht - von der Pflicht zur Wahrung eines ausgeglichenen Haushalts befreit ist.

Dienstag, 23. Dezember 2008

A primer on quantitative easing ...

... on video at vimeo. This link has the imprimatur of Greg Mankiw. More video coverage of the financial crisis can be found at marketplace.org/financialcrisis.

Sonntag, 21. Dezember 2008

Need more arguments against ZIRP?

Zero Interest Rate Policy (ZIRP) may be doomed to fail in stimulating a stumbled economy. The reason is that at zero rates financial intermediaries are not inclined or able to raise funds and to lend them out. But it is exactly this kind of business what the Fed needs to get the economy back on track. As the FT reports, ZIRP has taken money market funds hostage-perhaps the only remaining intermediaries that, until recently, continued to create market liquidity.

Samstag, 20. Dezember 2008

American Sonderweg?

While the European Union is working on tighter regulation of hedge funds (see previous post), the Federal Reserve will effectively start acting as a prime broker for them, as the Financial Times reports: Hedge funds gain access to $200bn Fed aid. For a critical discussion, see also the corresponding entry in the investment banker blog naked capitalism with further links.

Hedge funds' access to Federal Reserve credit will take place in the context of TALF, the Term Asset-Backed Securities Loan Facility. (Fed's Press Release on the new rules for TALF.) In opening TALF for hedge funds, the Fed will help them get the leverage they need for their business model. In effect, the Fed will help hedge funds to stay alive in an environment that has become increasingly hostile for them. More on hedge funds' problems in times of the credit crunch can be found in FAZ: Kampf um die Zukunft.

This brings me to my question: Why keep hedge funds alive with public funds? I say: Don't do it! Let them wither away and die a natural death. Let them become the dinosaurs of economic evolution. One less problem to worry about.

Hedge funds' access to Federal Reserve credit will take place in the context of TALF, the Term Asset-Backed Securities Loan Facility. (Fed's Press Release on the new rules for TALF.) In opening TALF for hedge funds, the Fed will help them get the leverage they need for their business model. In effect, the Fed will help hedge funds to stay alive in an environment that has become increasingly hostile for them. More on hedge funds' problems in times of the credit crunch can be found in FAZ: Kampf um die Zukunft.

This brings me to my question: Why keep hedge funds alive with public funds? I say: Don't do it! Let them wither away and die a natural death. Let them become the dinosaurs of economic evolution. One less problem to worry about.

Donnerstag, 18. Dezember 2008

Commission launches public consultation on hedge funds

Today, the European Commission has launched a wide-ranging public consultation on hedge funds. It asks for views on problems such as systemic risks, market integrity and efficiency, risk management and transparency. The text of the consultation can be found here. This consultation must be seen in context with a resolution of the European Parliament of September 23, 2008, which has called for a tighter regulation of hedge funds and private equity. The resolution had been prepared by reports by Poul Nyrup Rasmussen and Klaus-Peter Lehne. It remains to be seen whether the activities of the Parliament and the Commission will result in a European hedge fund regulation.

Dienstag, 16. Dezember 2008

Why does the ECB hesitate to further slash its policy rates?

The WSJ reports on differences between the Fed and the ECB: While the former is keen to drive Fed Funds Target Rate to zero, the Europeans are less inclined to further decrease policy rates - at least not as fast as they did since October. Incomprehension prevails about the ECB's apparent reluctance. But the Japanese experience taught us the following (BIS Working Paper No. 188). On page 16 the authors write:

More importantly:

While the second reason may not hold under current conditions (credit spreads have substantially widened since Lehman), the first one is striking: when a central bank wants financial institutions to lend again to each other, policy rates at zero bound may be detrimental!

Under the QEP [Quantitative Easing Policy], financial institutions have increased their dependence on the BOJ’s [Bank of Japan] money market operations as a means of adjusting their reserve balances. The financial institutions with a funds shortage have become more dependent on the BOJ’s funds-providing operations, while those with a funds surplus have come to use the BOJ’s funds-absorbing operations as a means of investing funds. Put differently, the BOJ has come to play the role of a money broker. This is the mechanism through which the BOJ has provided ample liquidity. However, when concerns over the financial system’s stability have receded and the precautionary demand for liquidity has declined, the BOJ has often faced difficulties in its attempt to supply liquidity. Specifically, it has experienced undersubscriptions in fund-providing operations: the total amount of bids have fallen short of the amount offered by the BOJ even at the lowest bidding interest rate of 0.001%.

More importantly:

As financial institutions have become more dependent on the BOJ’s money market operations, the size of the call market [...] has contracted further [...] This reduction in the size of the call market reflects lowered trading incentives for the following two reasons: first, the returns on investment in the call market have declined to a level that cannot cover trading costs [...]. Second, credit spreads have been narrowed substantially. A call rate of 0.001% means that the average of all borrowing rates is 0.001%, leaving little room for differences in rates between individual borrowers.

While the second reason may not hold under current conditions (credit spreads have substantially widened since Lehman), the first one is striking: when a central bank wants financial institutions to lend again to each other, policy rates at zero bound may be detrimental!

Montag, 8. Dezember 2008

Econobloggers...

...are just about to change the way of policymaking. If someone looks for a good reason for blogging, see here.

Samstag, 6. Dezember 2008

Rescue Plan for American Automakers

The U.S. congress stands ready to bail out the auto industry by planning a series of loans to detroit carmakers. These loans are going to be associated with close government oversight to make sure that they will actually be used to reorganize the companies and to make them prepared for competition both in terms of costs and products. Nancy Pelosi, speaker of House of Representatives, said in a statement that “Congress will insist that any legislation include rigorous and ongoing oversight to guarantee that taxpayers are protected and that resources are directed to ensure the long-term viability and competitiveness of the American automobile industry.”

I merely wonder whether the U.S. officials are just about to declare that capitalism has failed. Those who are familiar with the reasons for the current misery in the U.S. auto industry may ask two questions: First, why did the industry not already take the required measures in recent years? Second, why has government to step in and to help the auto industry just in the mid of a financial crisis?

Maybe, answers can be found in Neo-Schumpeterian growth economics. To the first question: as long as the economy has boomed, marginal returns on investments in human capital intensive inventions, innovative and cost-reducing technologies have been small compared to those on investment in increasing capacity (for the simple reason that meeting the high demand in the boom is of first priority). To the second: When the economy stumbles and finds itself in a recession, the former kind of investment is more valuable than the latter one. Owing to dried up company-internal funding sources in these times, those investments have to be financed externally which is rather hard even in normal times because human capital is often not a good collateral for lending. But when there is also a financial crisis around, raising funds for those purposes is almost impossible.

While the second answer seems to be well-suited for the current problems in U.S. auto industry, one may still doubt that the answer to the first question is right.

I merely wonder whether the U.S. officials are just about to declare that capitalism has failed. Those who are familiar with the reasons for the current misery in the U.S. auto industry may ask two questions: First, why did the industry not already take the required measures in recent years? Second, why has government to step in and to help the auto industry just in the mid of a financial crisis?

Maybe, answers can be found in Neo-Schumpeterian growth economics. To the first question: as long as the economy has boomed, marginal returns on investments in human capital intensive inventions, innovative and cost-reducing technologies have been small compared to those on investment in increasing capacity (for the simple reason that meeting the high demand in the boom is of first priority). To the second: When the economy stumbles and finds itself in a recession, the former kind of investment is more valuable than the latter one. Owing to dried up company-internal funding sources in these times, those investments have to be financed externally which is rather hard even in normal times because human capital is often not a good collateral for lending. But when there is also a financial crisis around, raising funds for those purposes is almost impossible.

While the second answer seems to be well-suited for the current problems in U.S. auto industry, one may still doubt that the answer to the first question is right.

Freitag, 5. Dezember 2008

Worried about the crisis? Have some inflation!

Two renowned US economists are arguing that inflation is the best way to combat the financial crisis. In their article on the webpages of the Peterson Institute for International Economics they argue that inflation (i) is preferable to deflation and (ii) in times of crisis has many advantages of its own. One of the advantages - according to them - is that inflation in the US induces a depreciation of the US dollar vis-à-vis the euro and thus effectively forces the ECB to engage in a more expansionary monetary policy (whereas in the case of a fiscal stimulus in the US the Europeans would free ride on the US expansion).

If this is a representative opinion among US economists then within the next few months we will see a huge fiscal expansion in the US (announced: fiscal stimulus of up to $700bn) accompanied by a massively expansionary monetary policy deliberately aimed at generating inflation.

My recommendation to the rest of the world: Tighten your seat belts!

PS: One of the two authors is Simon Johnson.

If this is a representative opinion among US economists then within the next few months we will see a huge fiscal expansion in the US (announced: fiscal stimulus of up to $700bn) accompanied by a massively expansionary monetary policy deliberately aimed at generating inflation.

My recommendation to the rest of the world: Tighten your seat belts!

PS: One of the two authors is Simon Johnson.

Montag, 1. Dezember 2008

How (not) to combat a banking crisis

The Latvian authorities are testing a new approach to combat the financial crisis, as the Wall Street Journal reports: Overly pessimitic university teacher arrested. Honestly, I prefer the more traditional approach using monetary and fiscal policy. (Hier auf Deutsch)

Abonnieren

Posts (Atom)